https://apnews.com/article/crime-trending-news-government-and-politics-6f30f575dc739415af1e5b47b1be50f0

>>>

I personally believe that a lot more like activities occur to turn jails into cash cows all across America.

https://apnews.com/article/crime-trending-news-government-and-politics-6f30f575dc739415af1e5b47b1be50f0

>>>

I personally believe that a lot more like activities occur to turn jails into cash cows all across America.

Enjoying the flexibility to travel abroad, yet having the law office with us.

52 Foot Yacht, 950 hp.

1988 Jefferson Monticello 52′, 60,000 lb.

https://www.thehulltruth.com/galati-yacht-sales/466215-1988-52-jefferson-monticello-yacht-sale.html

“ACTA” is a Fantastic Motor Yacht, Perfect for Cruising or as a Live-A-Board Yacht. If you have ever Considered Experiencing the Adventure of America’s Great Loop Trip, “ACTA” can make this possible. Having three Staterooms and three Heads you have the option of how many guest you want onboard. The Master Stateroom if Full Beam with an Ensuite Head that has a Tub. The Electronics include a Chart Plotter, Radar, Bottom Depth Graph, VHF radio and more.

Pictures below:

Click on the picture to go to next picture.

(More to come.)

>>>>

Hansen’s comments – there are tracking requirements for individual instruments that these registered entities must follow to maintain legal standing to foreclose on individual notes. Essentially they must prove chain of title (owner). Contact pauljjhansenlaw@gmail.com for the process to do this with any note you may have suspicions about.

>>>>

The Securities Act of 1933 has two basic objectives:

To require that investors receive financial and other significant information concerning securities being offered for public sale; and

To prohibit deceit, misrepresentations, and other fraud in the sale of securities.

The SEC accomplishes these goals primarily by requiring that companies disclose important financial information through the registration of securities. This information enables investors, not the government, to make informed judgments about whether to invest in a company’s securities. Here’s an overview of how the registration process works. In general, all securities offered in the United States must be registered with the SEC or must qualify for an exemption from the registration requirements. The registration forms a company files with the SEC provide significant information, including:

A description of the company’s properties and business;

A description of the security to be offered for sale;

Information about the management of the company; and

Financial statements certified by independent accountants.

Registration statements and prospectuses become public shortly after the company files them with the SEC. All companies, domestic and foreign, are required to file registration statements and other forms electronically. Investors can then access registration and other company filings using EDGAR.

Not all offerings of securities must be registered with the SEC. The most common exemptions from the registration requirements include:

Private offerings to a limited number of persons or institutions;

Offerings of limited size;

Intrastate offerings; and

Securities of municipal, state, and federal governments.

By exempting many small offerings from the registration process, the SEC seeks to foster capital formation by lowering the cost of offering securities to investors.

The SEC’s Division of Corporation Finance may examine a company’s registration statement to determine whether it complies with our disclosure requirements. But the SEC does not evaluate the merits of offerings, nor do we determine if the securities offered are “good” investments.

While SEC rules require that companies provide accurate and truthful information, the SEC cannot guarantee the accuracy of the information in a company’s filings. In fact, every year the SEC brings enforcement actions against companies who have failed to provide important information to investors. Investors who purchase securities and suffer losses should know that they have important recovery rights if they can prove that there was incomplete or inaccurate disclosure of important information.

Territorial Jurisdiction Challenge.

>>

In The United States District Court

For The District Of Alaska

Plaintiff,

vs.

Defendant

)

)

)

)

)

)

)

)

)

)

Case No.: No. 12-3-456789-1

Brief in Support of Motion to Dismiss Indictment

This brief will outline the reasons this Court should dismiss the Indictment in this matter.

The Government in this indictment failed to plead a violation of any statute or regulation that would trigger the punishment statues cited in the indictment. The Government plead violation of 26 U.S.C. §7201. Attempt to evade or defeat tax., §7206 and §7203 along with certain sets of actions and circumstances. There are no duties involved with these statutes, only penalties. These statutes by their plain language address “any tax imposed by this title”. Title 26 contains every type of tax that any person in any taxable activity could be libel for in the United States. Until the government pleads in particular and with specificity which statutes that impose a tax along with the regulations that give them force of law that imposes a legal duty on the Jensens, there would be no possible way the Jensens, could prepare a defense or even know the theory of the governments case.

A defendant is entitled to know the theory of the governments case.

“A defendant is not entitled to know all the Evidence the government intends to produce, but only the Theory of the government’s case.” Yeargain v. United States, 314 F.2d at 882 (9th Cir. 1963).

Until there is a statue and regulation plead that causes the actions and circumstances plead in the indictment to operate in violation of the law this court cannot find the Jensens guilty of any illegal act. This type of pleading, while being very convenient for the Government, is very prejudicial and operates to deny the Jensens the right of being informed of the basis for the charges against them. This set of circumstances also operates to deny this court jurisdiction over the indictment.

While the Government took the time to identify in Count 1 a tax allegedly owed by Jensen as “the tax, penalties and interest due and owing by him”. The Government never did take the time to plead or identify a taxing statute along with it’s implementing regulation that creates the legal duty to pay such tax or file some tax form. Because 28 U.S.C. 2201(a) prevents the court from making any determinations concerning the Jensens taxpayer status these glaring omissions operate to deny this Court the ability to provide Finality of Judgment.

Revenue cases are unique in the jurisprudence of the United States and need to be plead in a unique fashion. 28 U.S.C §2201(a) prevents the court from making any determinations concerning the taxable status of the Jensens. So the Jensens come to court in this matter with the presumption of innocence and that there is not even a legal relation between the Jensens and any of Title 26. The burden is on the Government to plead with particularity and then prove what the Jensens legal relations is with some specific statute and regulation in order to prove they violated some legal duty. The only authority who can make that taxpayer status determination is the Secretary of the Treasury or his delegate. Under the present set of circumstances the Secretary of the Treasury or his delegate could appear at the trial and declare that the Jensens were not “Taxpayer’s” as defined. At that time the Court would have no option but to dismiss the case for lack of jurisdiction. Well those same circumstances exist RIGHT NOW… before the trial starts. Until such time as the government either supplies the record with an affidavit from the Secretary of the Treasury outlining the legal relations that the Jensens have with Title 26 or pleads in their indictment the legal relations with a particular statute and regulation that imposes a legal duty this court does not have all the Jurisdictional Elements that would give the court jurisdiction over the indictment. Anytime before the end of this impending trial if these errors are not cured all the courts decisions could be overturned by a executive agency. Thereby, rendering this Court powerless.

The combination of 28 U.S.C. §2201(a) and the lack of the proper affidavits from the Secretary of the Treasury or his delegate, or a properly plead indictment outlining the Jensen’s legal relationship with Title 26 operates to deny the Court any Judicial power. See United States Constitution Annotated Art, III “Finality of Judgment as an Attribute of Judicial Power,” Page 633, 1982 ed.

The Government has worked a fraud on the Grand Jury and is attempting to work that same fraud on the Court and the Jensens. In order to meet the required jurisdictional elements that the illegal acts took place under the jurisdiction of this Court the Government pled that the Jensens committed the illegal acts alleged in the indictment “in the District of Alaska and elsewhere”.

One of the key jurisdictional elements of a Federal Crime is the place it was committed. Until the Government can plead unchallenged or prove the defendants where actually in some “District of Alaska” or some other place under exclusive Federal jurisdiction referred to as “elsewhere” this court does not have all the jurisdictional elements to provide for proper jurisdiction over the indictment. See United States v. Spinner, 180 F.3d 514 (3rd Cir. 1999).

The facts recited by the government state that the Jensens lived in Cordova Alaska. Cordova is a small isolated fishing town in Alaska and does not comprise any generally known Federal District. If the Government wants to plead that Cordova Alaska is included in some kind of generally unknown “District of Alaska” they need to plead the legal relation between the Jensens and said Federal District so that the Jensens can know the theory of the governments case, they can craft a proper defense and this Court will have proper jurisdiction.

The Court is well aware of what it takes to have proper jurisdiction. Jurisdiction over, the subject matter, the place, and the person. It takes all three for the court to have all the jurisdictional elements that grants jurisdiction over the indictment. As the court can see this indictment is fatally flawed in many respects. The Government Department of Justice wields great power and employs more well educated attorneys than any business in America. The Government knows how to do indictments correctly and its the Courts duty to force them to do their jobs correctly. This type of procedure is just one step from just having a government agency pick up a person and take them straight to jail without any due process or court process.

If the court dismisses this fatally flawed indictment nothing is stopping the Department of Justice from starting over and getting the process correct. For the foregoing reasons the Jensens ask that the indictment in this matter be dismissed.

Dated this 29th day of April, 2012

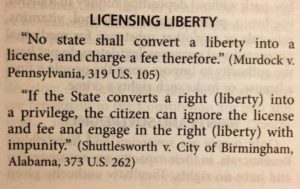

Immunity > judicial, sovereign, official, prosecutorial, personal.

LEWIS ET AL. v. CLARKE CERTIORARI TO THE SUPREME COURT OF CONNECTICUT No. 15–1500. Argued January 9, 2017—Decided April 25, 2017

(1.) But sovereign immunity “does not erect a barrier against suits to impose individual and personal liability.” Hafer, 502 U. S., at 30– 31 (internal quotation marks omitted); see Alden v. Maine, 527 U. S. 706, 757 (1996).

(2.) Supreme Court Strikes Down Qualified Immunity Claim – Ep. 7.276,

Cases COULD mean a shift in the court’s attitude toward the qualified immunity doctrine they created.

https://www.abajournal.com/columns/article/chemerinsky-scotus-hands-down-a-rare-civil-rights-victory-on-qualified-immunity

Territorial Jurisdiction Evidence of Law:

(1.) Catha v United States , 152 US , at 215

U.S. Code, Title 28 – JUDICIARY AND JUDICIAL PROCEDURE, (Chapter 176) Section 3002 (15) (a, b, & c) THINK ART1, SEC.8, CL17. “The laws of Congress in respect to those matters do not extend into the territorial limits of the states, but have force only in the District of Columbia , and other places that are within the exclusive jurisdiction of the national government.”

(2.)

What the IRS refused the Jury to see, would completely proven ‘no intent‘ for Defendant Hird.

Denial of a fair trial.

Denial of a defense.

Denial of placing your evidence before the jury.

They also denied Paul John Hansen as a witness as to what Thomas Hird relied upon as 10 years of notice upon the IRS as to his request if he is required to file a 1040 U.S. Individual Income Tax Return for any given year.

See court filed document below that was bared from the jury, and the questions and testimony of Paul John Hansen, that was also barred.

#71 XXX DEFENCE DISCOVERY ENTRY

(Comment by Hansen – the below was sent me by a friend, I have not reviewed all of it but it looks of value.)

“In 1887, Congress passed the Tucker Act (24 Stat. 505), which further restricted the claims that could be submitted directly to Congress and required the claims instead to be submitted to the Court of Claims. It broadened the court’s jurisdiction so that “claims founded upon the Constitution” could be heard. In particular, this meant that monetary claims based on takings under the eminent domain clause of the Fifth Amendment could be brought before the Court of Claims. The Tucker Act also opened the Court to tax refund suits.

Depredations against American shipping committed by the French during the Quasi-War of 1793 to 1800 led to claims against France that were relinquished by the terms of the Treaty of 1800. Since the claims against France were no longer valid, claimants continually petitioned Congress for the relief that had been waived by the treaty. Only on January 20, 1885, a law was passed, 23 Stat. 283, to provide for consideration of the matter before the Court of Claims. The lead case, Gray v. United States, 21 Ct. Cl. 340, written by Judge John Davis, includes a complete discussion of the historical and political circumstances that led to the hostilities between the United States and France and their resolution by treaty. The cases, termed “French Spoliation Claims”, continued in the court until 1915.

In 1925, Congress changed the structure of the Court of Claims by authorizing the Court to appoint seven commissioners who were empowered to hear evidence in judicial proceedings and report on findings of fact. The judges of the Court of Claims would then serve as a board of review for the commissioners.

In 1932, Congress reduced the salary of the judges of the Court of Claims as part of the Legislative Appropriation Act of 1932. Thomas Sutler Williams was one of the judges of the Court, and he sued the federal government by claiming that his salary could not be cut because the Constitution had specified that judicial salaries could not be reduced. The Supreme Court ruled on Williams v. United States in 1933, deciding that the Court of Claims was an Article I or legislative court and so Congress had the authority to reduce the salaries of the judges of the Court of Claims.[6]

Beginning in 1948, Congress directed that when directed by the court, the commissioner could make recommendations for conclusions of law (62 Stat. 976). Chief Judge Wilson Cowen made that mandatory under the court rules in 1964.”

And that ACT opened the doors for what now exists as the United States Court of Claims.

[The United States Court of Federal Claims (in case citations, Fed. Cl. or C.F.C.) is a United States federal court that hears monetary claims against the U.S. government. It is the direct successor to the United States Court of Claims, which was founded in 1855, and is therefore a revised version of one of the oldest federal courts in the country].

One of THE oldest federal courts. Hmmmm

[Federal tribunals in the United States are those tribunals established by the federal government of the United States for the purpose of resolving disputes involving or arising under federal laws, including questions about the constitutionality of such laws. Such tribunals include both Article III tribunals (federal courts) as well as adjudicative entities which are classified as Article I or Article IV tribunals. Some of the latter entities are also formally denominated as courts, but they do not enjoy certain protections afforded to Article III courts. These tribunals are described in reference to the article of the United States Constitution from which the tribunal’s authority stems. The use of the term “tribunal” in this context as a blanket term to encompass both courts and other adjudicative entities comes from section 8 of Article I of the Constitution, which expressly grants Congress the power to constitute tribunals inferior to the Supreme Court of the United States.]

It clearly states that the Federal Court of Claims exists under “Article 1” constitutional authority. Above you will note it is NOT considered to be a COURT. Instead, it is termed “other adjudicative entities…” See section 8 of Article 1. This so called Claims Court is obviously meant to serve NCUSN’s that have been affected by state citizens under an INDIVIDUAL contract (State issued ID) as well as a contract to be paid wages for working under a contract that affords the person(s) very limited authority that is ONLY applicable when dealing with other citizens that are aboard that CITIZEN-SHIP. If you’re a citizen of the U.S., then all you set is THIS:

[The Federal Tort Claims Act (August 2, 1946, ch.646, Title IV, 60 Stat. 812, 28 U.S.C. Part VI, Chapter 171 and 28 U.S.C. § 1346) (“FTCA”) is a 1946 federal statute that permits private parties to sue the United States in a federal court for most torts committed by persons acting on behalf of the United States. Historically, citizens have not been able to sue their state—a doctrine referred to as sovereign immunity. The FTCA constitutes a limited waiver of sovereign immunity, permitting citizens to pursue some tort claims against the government.]

AND, the citizenry is limited to a CAP…

[This cap is only increased in cases of catastrophic loss or injury, and even then the injured party is limited to $1,000,000 in non-economic damages. The FTCA prohibits punitive damages from being awarded against the government. … Instead, only compensatory damages can be awarded in an FTCA case.]

The % of wins for the citizenry is very low in my estimation. In fact, I bet no one really wins there except the federal employees of the courts and doj along with all the BAR licensed attorneys that have their hands in that cookie jar. I SEE the deception so clearly now, y tu?

Whats even clearer now is THE REMEDY we now have as NCUSN status holders…amazing how well THE COURT CLERKS are cooperating with the Nevada Open Records Act DEMANDS that were sent about 3 weeks ago. They’re running out of time. Punitive AND compensatory damages are payable to NCUSN’s with VALID CLAIMS…now

Contact us, we can formulate actions that may make you tens of thousands by forcing the any city, county, or state, in the United States, to admit they are depriving you of a right.

Congress has never authorized the operation of the IRS as a matter of law, some state that it is as a matter of necessity, and not specific law.

Click on the image to enlarge.

https://www.irs.gov/irm/part1/irm_01-001-001#idm139964655721888